By Akiko Inoguchi and Lyndall Bull

Lower Mekong in transition: unpacking the trends of forest trade

FAST READ

- Regional dynamics of investment and trade play an important role in determining land use change. They can act as drivers of forest degradation and deforestation or they can shift these trends positively.

- In this article, authors Akiko Inoguchi and Lyndall Bull investigate the evolution of trade in primary and secondary wood products within the Lower Mekong.

- By understanding the drivers of intra- and extra-regional trade in wood products, we can develop more targeted policies to minimise illegal harvesting, illegal trade and their impacts on forest degradation and deforestation. This can also help in the development of policies that support a legal and sustainable pathway for a robust forest industry in the region.

Introducing the countries

The five Lower Mekong countries fall into two distinct camps: Viet Nam and Thailand are wood processing and export hubs; and the remaining three countries (Lao PDR, Myanmar and Cambodia) are in transition from a forest sector based primarily on the export of unprocessed timber from natural forests to a more sustainable and robust forest industry based on plantations.

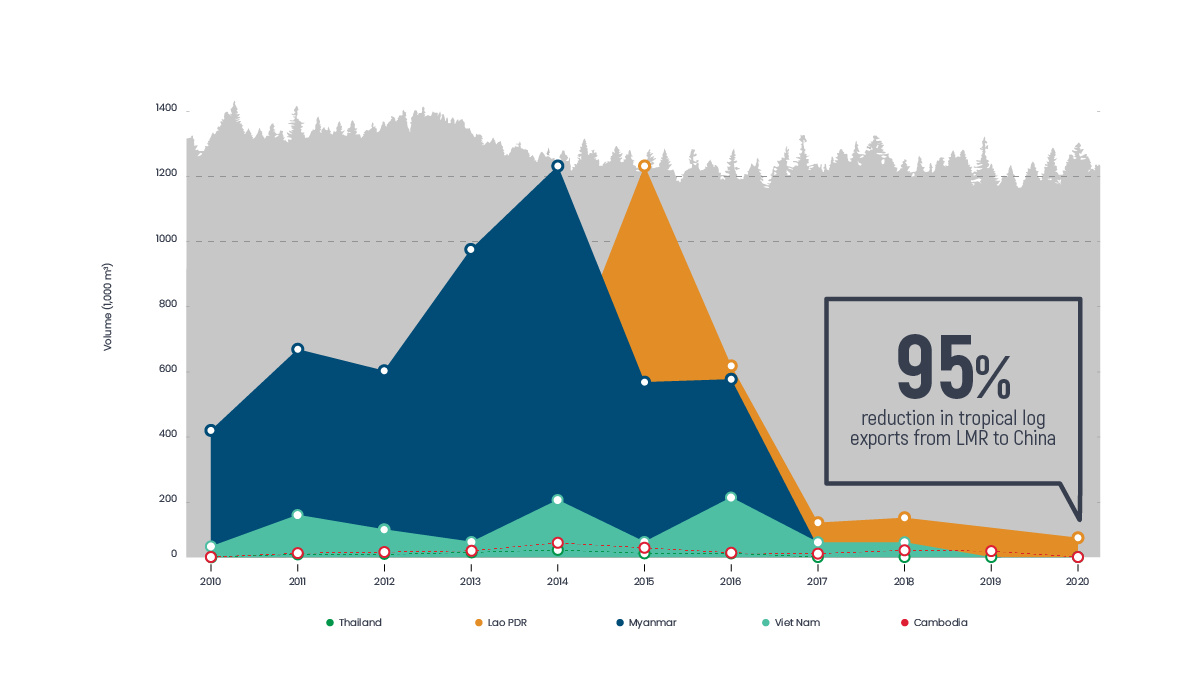

China looms in the background of all countries as an important, and until the recent past, a dominant destination for wood exports from Lower Mekong countries.

Figure 1: China imports of tropical logs (including plantations) from the Lower Mekong countries, by volume, 2010-2020, by country of origin

Introducing the Trends

The trade of wood products in the Lower Mekong has undergone significant change over the past decade with four dominant trends.

Decreased exports of primary wood products from natural forests

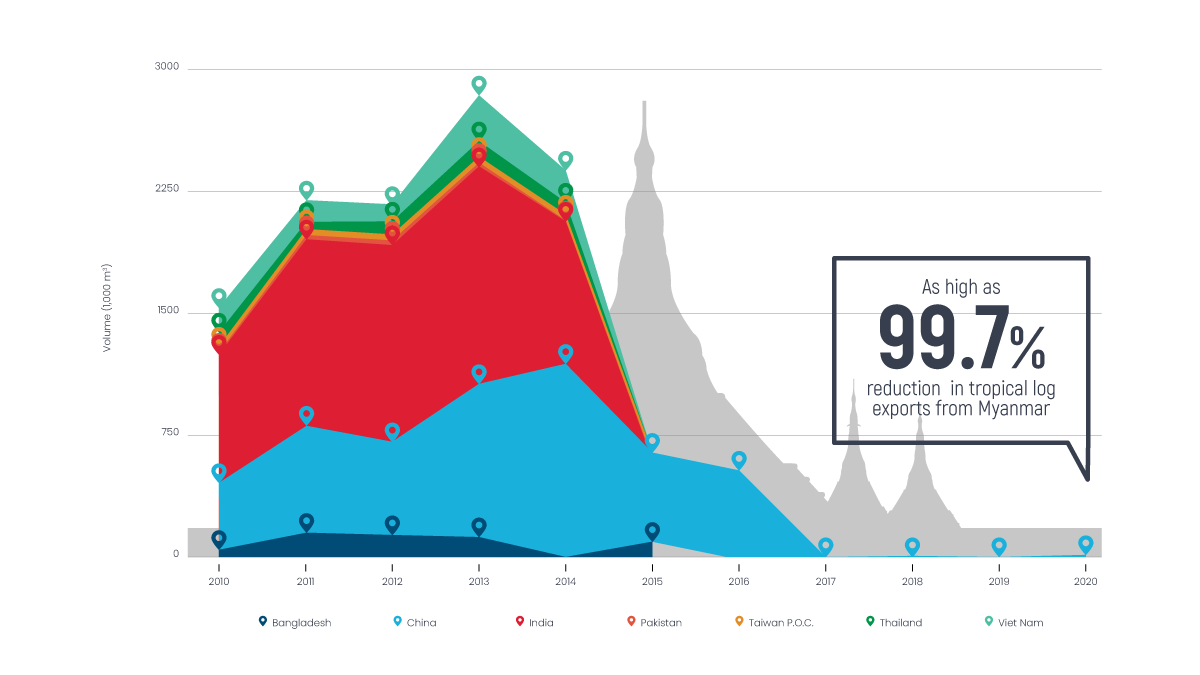

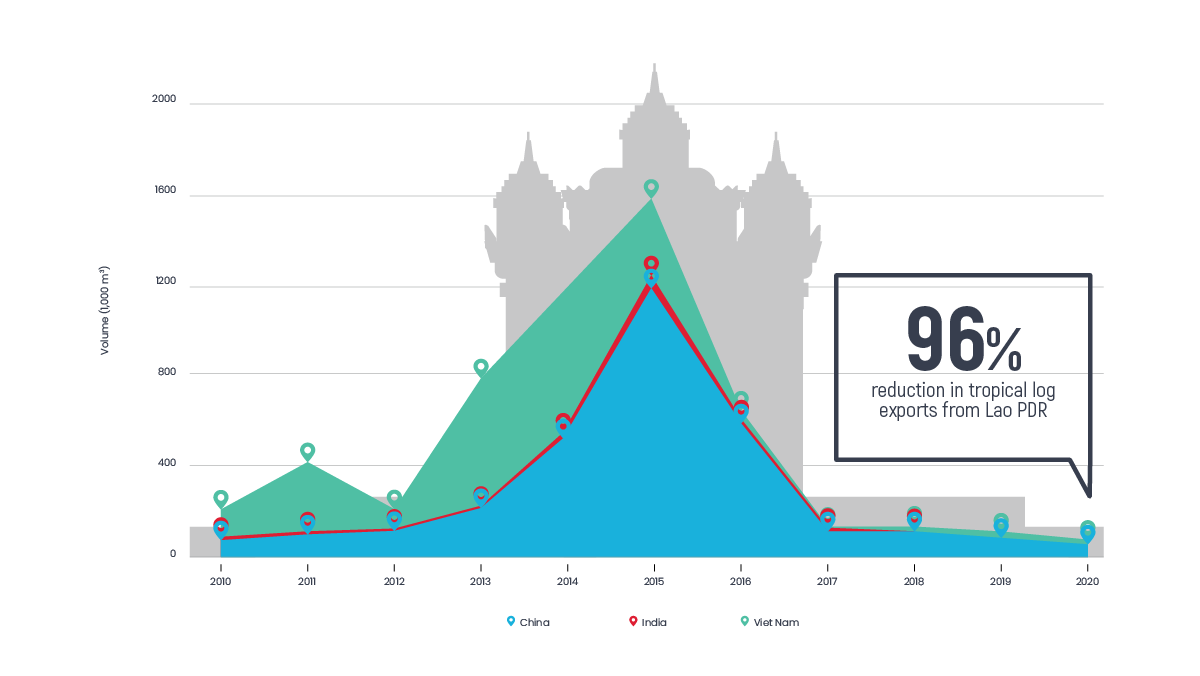

Over the last decade, there has been a dramatic plunge in the export of primary wood products sourced from the natural forests of Myanmar and Lao PDR. Log exports from the region totalled 3.5 million m3 and were valued at close to $2 billion US in 2013, the peak year. Since 2017, log exports have dropped to minimal levels from both countries. These trends indicate both sustainability concerns and opportunities.

Figure 2: Log exports by destination for:

(a) Myanmar

(b) Lao PDR

The primary driver of the plunge in exports is likely the exploitation and depletion of the resource base, particularly of commercially valuable species such as rosewood and natural teak. Much of the commercially valuable natural forest timber may have already been extracted. Whether or not this can be corroborated with data collected from the national forest inventories may be worth review.

The observed decline in production of primary wood products from natural forests may also be due to the effectiveness of national policies designed to decrease such trade.

In Myanmar, a log export ban, implemented in April, 2014, sought to increase domestic processors’ access to raw material. A ban was also imposed on other timber exports to increase the efficiency of enforcement by preventing cross-border trade. A one-year moratorium on logging across the country and a ban on non-competitive timber sales have also been imposed since 2016, restricting exports of logs.

In Lao PDR, policy instruments aimed at curbing unsustainable and illegal practices in natural forests have existed for some time. These instruments were intended to reduce deforestation and redirect the export of unprocessed wood products to support the development of the domestic wood processing industry; however, they generally had little effect. In 2016, the government issued Prime Minister Order 15 (PMO 15) which prohibited the export of unprocessed timber from natural forests and restricted domestic trade in wood products, including from plantations.

Optimistically, with these policy instruments in place, there may now be the resolve to increase the sustainable timber trade across the Lower Mekong.

In Lao PDR for instance, media reports on illegal logging related events might not have ceased, but have reduced in the past five years. However, political turmoil in Myanmar, combined with the COVID pandemic, suggest the need for continued vigilance.

The emergence of Viet Nam and Thailand as global hubs of wood products trade

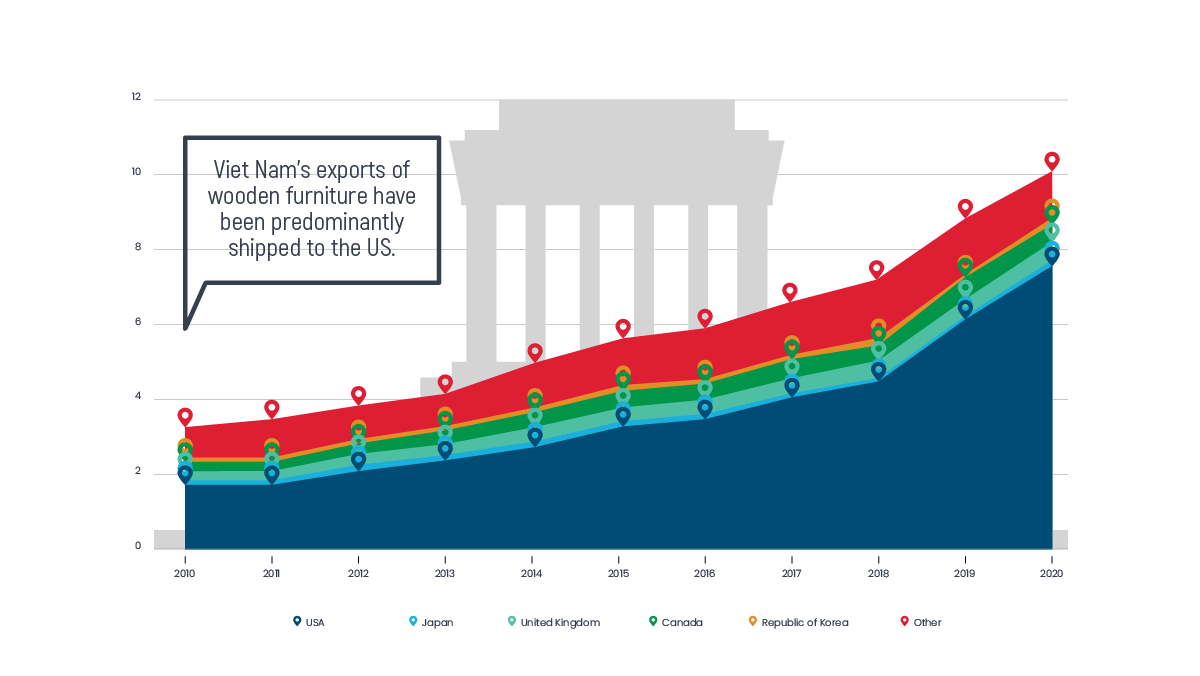

Viet Nam’s exports have surged over the last four years, with veneer predominantly shipped to China and tropical plywood and wooden furniture mainly to the United States. In 2020, with the country’s early control of the pandemic enabling a quick resumption of production and exports, Viet Nam was able to capture a surge in demand from the United States.

Exports are manufactured from a combination of domestic and imported fibre. Viet Nam’s imports of primary products from Lao PDR, Myanmar and Cambodia have declined considerably and have been replaced by supplies from the African region. There is, on the other hand, an increasing trend of forest trade in plantation timber and fibre, including from Lower Mekong sourcing countries.

Figure 3: Viet Nam: Exports of wooden furniture, by value, 2010-2020, by country of destination

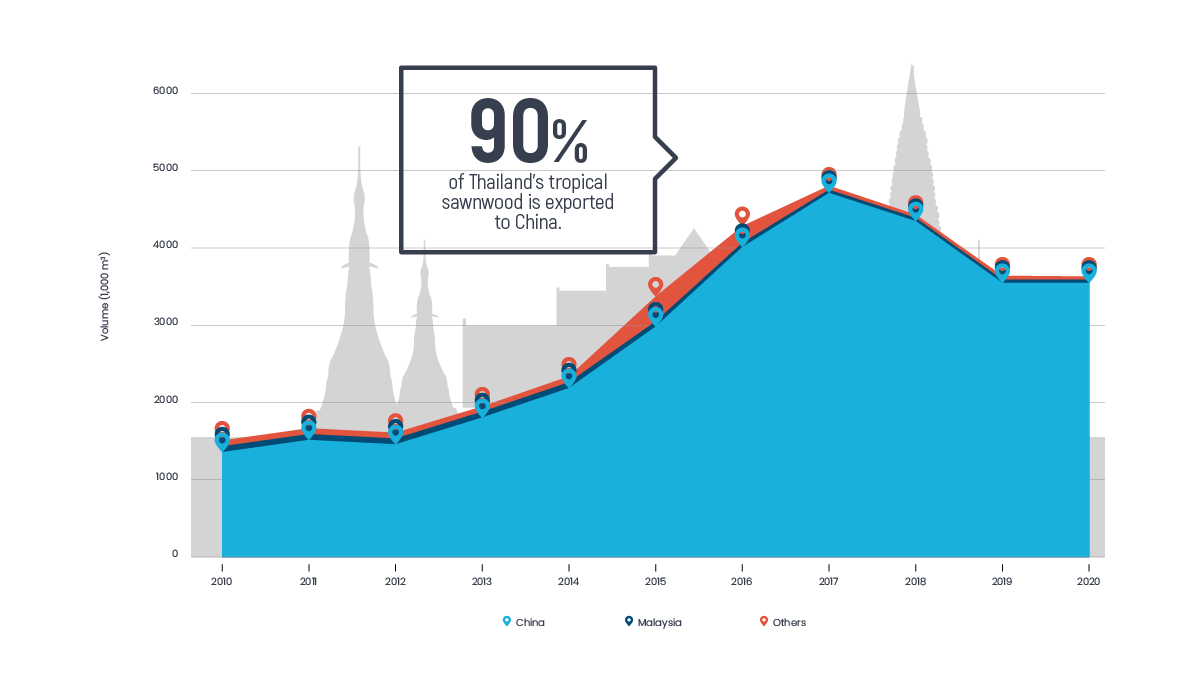

In Thailand, no legal timber harvests in natural forests have been allowed since 1989. The focus on domestic harvest has shifted to plantations. Thailand now has a strong export industry based on sawnwood produced from rubberwood plantations. These plantations cover more than 3.7 million ha, with 90% of production being exported to China, mainly as sawnwood (Figure 4) and to a lesser extent, wooden furniture. Thailand is also a major exporter of wood-based panels, particularly MDF and particleboard which are based on plantation grown wood, including rubberwood. In 2020, the rubberwood industry was severely impacted by Covid-19 restrictions in the furniture manufacturing industry in China.

Figure 4: Thailand exports of tropical sawnwood, 2010-2020, by volume, by country of destination

The ongoing importance of China in the regional wood products trade

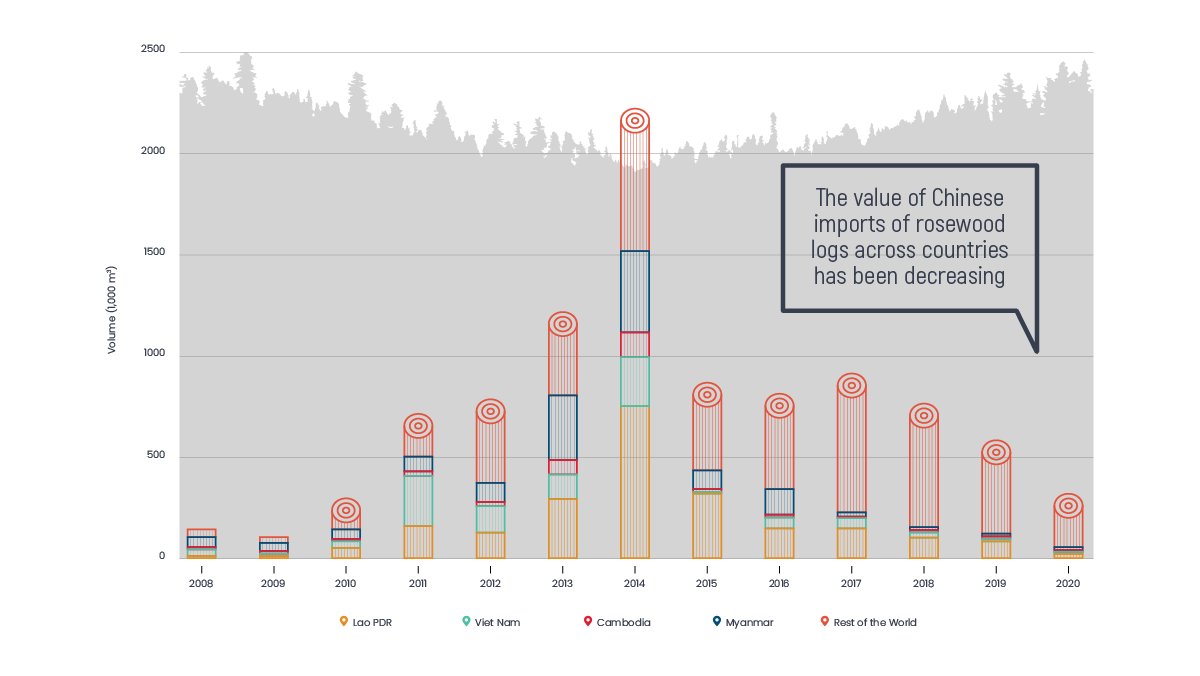

China is an important destination for many wood products produced in the LMR region because of both the significant domestic consumption of wood products and the size of the wood processing industry for re-export. One species of particular note is rosewood. China’s demand for LMR rosewood has been dampened in recent years by escalating prices, resulting in part from improved control on export of CITES-listed species and the availability of less costly substitute species from Africa.

Rosewood species that have been exported from LMR countries include Dalbergia cochinchinensis and Dalbergia oliveri, both of which have been listed in CITES Appendix II since 2016.

Figure 5. Value of China imports of “rosewood” logs by major country of origin, 2008-2020

Increasing the role of forest trade governance and certification to improve sustainable trade

Trade and forest governance mechanisms will need to be put in place in order to pave the way for a sustainable regional forest industry that is also a source of green jobs. While there is still a ways to go, there are positive signs that Myanmar, Lao PDR and Cambodia are moving in the right direction.

For example, in addition to exiting national policies, Lao PDR is making progress in its negotiations with the EU on a Forest Law Enforcement, Governance and Trade (FLEGT) Voluntary Partnership Agreement (VPA).

Cambodia and Myanmar have also been active in implementing their respective FLEGT action plans. Currently, timber from natural forests will mostly be outside the scope of sustainable trade, with the exception of conversion timber which remains a significant source of unsustainable timber.

Within the Lower Mekong, voluntary commitments from the forest industry on sustainable production and legal trade are increasing, including corporate actions to comply with international forest certification standards. As well, developments in all three countries are being made to advance the development of national forest certification systems and infrastructure.

*This article is based on the draft report by Fran Maplesden of ITTO.